Falling after a new high: Price stall, miners under pressure, and retail investors can actually buy coins for $90,000???

Key Takeaways

- Bitcoin Price Volatility: BTC’s rally stalled this week, with significant pressure above $110,000, including a wick down to $103,528. Risk-off sentiment boosted gold, but “digital gold” performed poorly.

- First Hashrate Adjustment Down: After seven consecutive increases, mining difficulty decreased by 3.2% for the first time, offering miners a brief reprieve.

- Miner Profit Pressure: Hashprice dropped to $47–$50/PH/day, pushing small and medium-sized miners close to the break-even point.

- TeraWulf Finances AI Computing Power: The crypto mining industry is seeking to pivot towards AI, with Wall Street capital continuing to pour in.

- Fed Minutes Release Dovish Signals: Market expectations shifted towards easing, but the coin price response was weak.

I. Market Overview

BTC Price Trend

This week, the Bitcoin price continued its sharp volatility. The sell-off triggered by macro events last weekend caused the price to briefly fall below the $110,000 mark, after which the market gradually stabilized near $111,000. Bitcoin lacked upward momentum this week and failed to break through previous resistance levels. Today, the price briefly dropped below $103,600, erasing this week's rebound gains.

Network Hashrate

This week, the Bitcoin network’s total hashrate remained in a historical high range, slightly below last month's peak level but still astounding. As of Friday, the 7-day average hashrate of the entire network rebounded to a level of about 1.10 ZH/s, approaching 1,100 EH/s. For most of the week, the network hashrate fluctuated between 1,000 and 1,150 EH/s. The average hashrate in the first two weeks of October was about 1,030 EH/s, a slight decrease of about 5 EH/s compared to the end of last month. This small decline is viewed as a natural adjustment after hashrate “overheating,” and is also related to some older mining machines being temporarily taken offline due to compressed profits. If the Bitcoin price fails to significantly strengthen, the decommissioning of high-operating-cost miners will cause the hashrate at high levels to exhibit some repetition and elasticity.

Transaction Fees

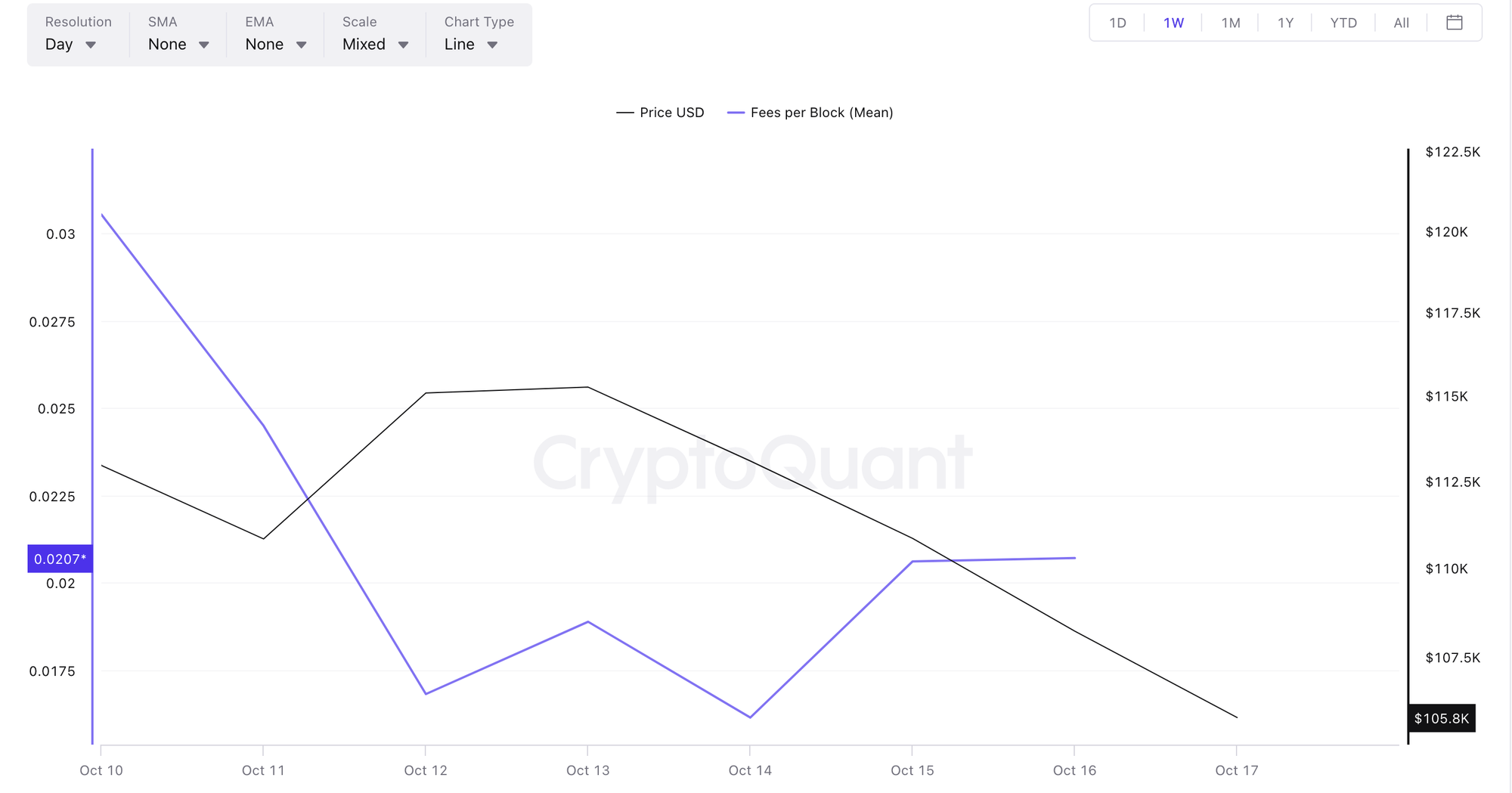

This week, the average Bitcoin transaction fee received by miners in BTC per block exceeded 0.03 BTC on October 10, indicating heavy network congestion and strong user willingness to pay at the time. However, the fee quickly dropped afterward, hitting a low point of about 0.017 BTC on October 12. Subsequently, the transaction fee fluctuated at a low level, finally stabilizing at about 0.02 BTC on October 15 and 16. Within the week, the revenue Bitcoin miners gained from transaction fees decreased compared to the start of the period.

Mining Difficulty

Bitcoin mining difficulty saw a rare downward adjustment this week, the first decrease in nearly ten months. On October 16, the Bitcoin network completed its difficulty cycle adjustment, with a downward adjustment of approximately 2.7%. After the adjustment, the network's total difficulty dropped from the previous approx. 150.84 T to about 146 T. This change ended the trend of seven consecutive difficulty increases since June this year. The previous seven difficulty cycles collectively increased the difficulty by about 50%.

For miners, this difficulty reduction is undoubtedly a "long-awaited breather," and the mining competitive environment may enter a brief period of rebalancing. The next difficulty adjustment is expected to occur around the end of October, with preliminary forecasts suggesting the difficulty may rise again by about 3-4%. Miners still need to pay attention to the dynamic balance between hashrate input and difficulty changes.

II. Market Analysis

Price and Output

This week highlighted the continued squeeze on miners' profit margins. Against the backdrop of high-level consolidation in coin prices and stubbornly high mining difficulty, the Bitcoin revenue miners obtain for every unit of hashrate invested is relatively reduced, and the fiat value of the unit output is also low. Hashprice is currently only around $47–$50/PH/day. This figure represents a significant drop compared to the level in the first half of this year, reflecting that even if the Bitcoin price remains near historical relative highs, mining revenue is diluted due to the soaring difficulty.

Hashrate Trends

The long-term growth trend of the Bitcoin network hashrate remained unchanged this week, although it experienced a slight adjustment after a period of rapid hashrate expansion. In the long term, with leaps in mining machine technology and large-scale capital investment, global Bitcoin hashrate has climbed all the way in 2025. Major mining companies have been deploying the latest generation of ASIC miners, improving energy efficiency and expanding capacity, causing the network hashrate to repeatedly hit new highs.

Among global listed mining companies, Marathon achieved a hashrate scale of 53.3 EH/s at the end of the third quarter, reclaiming the top spot among public companies; another mining giant, Bitdeer, saw its hashrate grow by 33% this quarter, jumping to the fifth largest miner. At the same time, traditionally leading mining companies like Riot, Core Scientific, and others are also continuously building new facilities and connecting new miners. The overall hashrate landscape is constantly being refreshed, and the hashrate investment of top players continues to climb rapidly.

Cloud Mining Market

This week, affected by the continuous pullback in the BTC price, sentiment in the cloud mining market was cautious. The nominal median quote for a 180-day cloud mining contract remained at approximately $0.0512/T/day (or $51.2/PH/day). Meanwhile, if an investor purchases a cloud mining product with a 720-day cycle at a mining price of $0.04/T/day, the effective acquisition cost of BTC through mining (i.e., the break-even coin price) is approximately $93,600.

III. News and Events

Macroeconomic and Policy Dynamics

International gold prices hit a new high this week, breaking through $4,300 per ounce, and silver prices also surged to record levels simultaneously. This indicates a decline in investor risk appetite and an influx of capital into safe-haven areas such as precious metals. However, Bitcoin did not strengthen synchronously during this wave of risk-off trading, instead stalling and pulling back, which to some extent weakened its “digital gold” safe-haven narrative.

The fuse that triggered the Bitcoin crash last weekend came from an escalation in US-China trade tensions. China announced new export restrictions on key rare earth metals, and President Donald Trump threatened to impose 100% tariffs on Chinese goods. This series of news caused global market volatility around October 10: stocks fell, risk assets were sold off, and Bitcoin was not spared.

The Federal Reserve's national economic conditions survey report, released on October 15, showed more signs of softening in the US labor market and slowing economic activity. This strengthened market expectations that the Fed might end its tightening cycle earlier or even begin cutting rates. Recent speeches by several Fed officials have also leaned dovish: Chair Powell mentioned the job market is “somewhat weak” and did not re-emphasize continued rate hikes; Minneapolis Fed President Kashkari expressed a wait-and-see attitude toward further hikes. CME's FedWatch interest rate futures tool shows that traders anticipate a high probability of the Fed cutting rates by 25 basis points before the end of this year. Easing expectations usually serve as a tailwind for assets like Bitcoin, as rate cuts imply improved liquidity and lower risk-free rates.

Mining Events

US-listed mining company TeraWulf Inc. announced on October 14 that it plans to issue $3.2 billion in Senior Secured Notes to raise capital for expanding its Bitcoin mining data centers and growing its High-Performance Computing (HPC) business. Remarkably, this bond financing received support from tech giant Google. Bloomberg reported that Google will participate as a strategic partner to endorse the deal, a first in the crypto mining industry. The market interprets this as an indirect recognition by a major technology company of the value of Bitcoin mining infrastructure. Spurred by the news, TeraWulf's stock (NASDAQ: WULF) surged significantly this week, with a cumulative gain of approximately 28%. If successfully issued, this $3.2 billion financing would be one of the largest single financings in the crypto mining sector, far exceeding previous fundraising records by mining companies.

Accompanying this year's Bitcoin price increase and the strong mining fundamentals, mining company stocks have performed brightly in the capital market. As of mid-October, the total market capitalization of the world's 15 major Bitcoin mining companies reached approximately $90 billion, a significant increase from a month ago.

It is necessary to remind investors that mining stocks typically have a high Beta characteristic, meaning that Bitcoin price movements are reflected in an amplified way in the stock price. Therefore, the rise in mining stocks this week also reflects the market's relatively bullish sentiment towards the future of Bitcoin. However, once the coin price sees a significant pullback, mining stocks may face more violent volatility.

Renewable Energy and Mining Layout

This year, the state of Texas in the US signed a bill supporting the establishment of a state-level Bitcoin strategic reserve and also introduced multiple policies encouraging the integration of the mining and energy industries. For example, Texas is attracting solar and wind power generation projects to power data centers, and some local governments offer tax incentives to draw in large mining farms. Meanwhile, in regions with abundant oil, gas, and solar resources, such as the Middle East and Central Asia, companies are also utilizing surplus energy for Bitcoin mining. According to industry analysis, the large-scale flexible load connected to the grid in Texas (mainly contributed by Bitcoin mining farms) is projected to reach 9.5 GW by the end of 2025, accounting for about 10% of the state's peak load.

{kind=link}