Hashrate Hits a New Level! Entering Zettahash – Can Miners Still Make Money?

Bitcoin Hashrate Market Weekly Report (September 6 – September 12, 2025)

Key Highlights

- Price: This week, BTC initially stabilized and then rose, trading overall in the $110,000–$115,000 range. Midweek, it broke above $114,000, but the upward momentum slowed, and the weekly close was slightly higher. Combined with expectations of macroeconomic interest rate cuts, BTC price could potentially target $150,000.

- Hashrate and Difficulty: The 7-day average hashrate remained above 1 ZH/s (1,000 EH/s), with the overall network hashrate continuously reaching new highs. Current difficulty is around 136 T, and the next adjustment, expected in mid-September, may increase by approximately +7%. However, seasonal hashrate fluctuations during winter could disrupt the upward trend.

- Macro: The U.S. Department of Labor’s annual benchmark revision significantly downgraded nonfarm payrolls over the past year; for August, nonfarm payrolls increased by only 22,000, with an unemployment rate of 4.3%. Coupled with a PPI YoY of 2.6% (below expectations) and a CPI YoY of 2.9% (in line with expectations), this clears the way for the Federal Reserve to begin a rate-cutting cycle.

- Industry: Dogecoin has notably secured approval for an ETF. Some cryptocurrency ETF approvals remain cautious, with a short-term impact on prices being neutral to slightly positive.

I. Market Overview

1) BTC Price

BTC traded in a range-bound uptrend.

- Sept 5: Ahead of NFP, BTC surged from ~$110k to ~$113k. The weak jobs report (+22k NFP, 4.3% unemployment) pushed prices briefly higher before retracing to ~$110k.

- Sept 9: Another push toward ~$113k met resistance.

- Sept 10: Weaker-than-expected PPI (2.6% YoY) triggered a rally from ~$112k to ~$114k, holding above this prior resistance.

Overall, BTC fluctuated between $110k–115k, heavily influenced by macro data, with downside cushioned by rate-cut expectations.

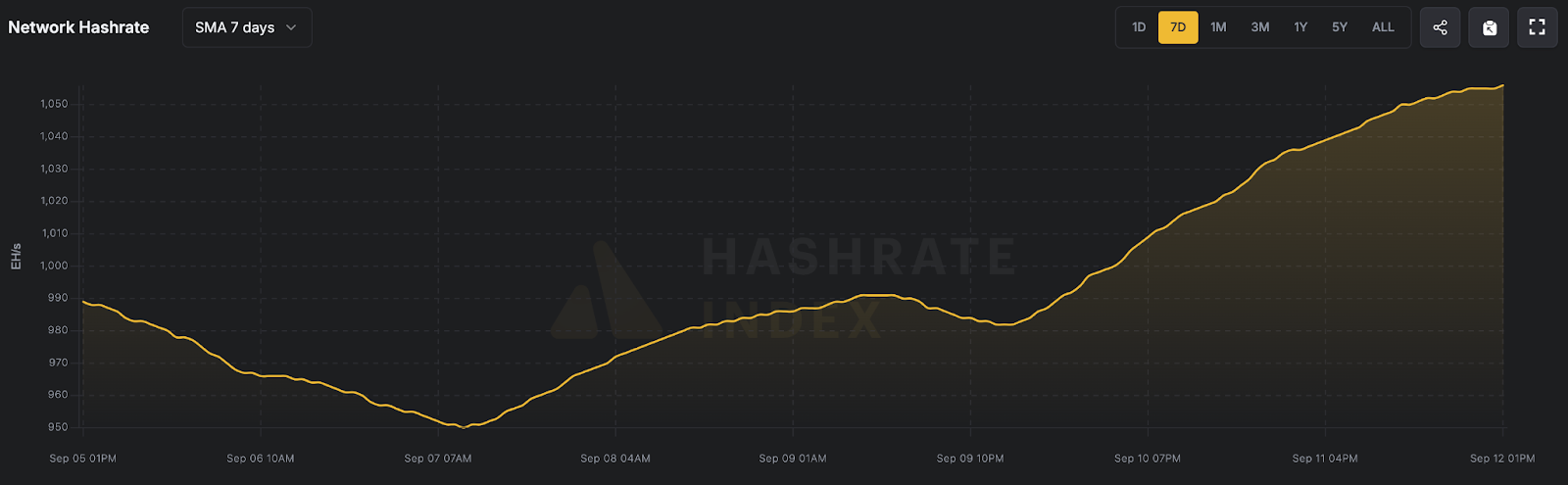

2) Network Hashrate

Hashrate continued climbing, with the 7-day average breaking above 1 ZH/s for the first time, signaling a new era for mining. Daily hashrate fluctuated between 900–1,050 EH/s. While this enhances network security, it reduces BTC rewards per unit of hashrate, squeezing higher-cost miners.

3) Mining Difficulty

Currently at a record ~136T. Based on block times, the next adjustment (mid-September) is expected to rise by about +7%. This would further reduce BTC output per TH/s, strengthening the competitive edge of efficient, low-cost miners.

II. Market Analysis

1) Price–Mining Profitability

With BTC holding above $110k, miners enjoy modest profit margins.

- Average mining cost per BTC: ~$99k.

- Spot BTC (~$112k) leaves about 10% gross margin.

But with difficulty climbing, hashprice (daily revenue per PH/s) remains at $53–55, lower than last month. Transaction fee revenue is minimal, leaving miners dependent on block rewards.

Historically, when miner profitability approaches breakeven, it often signals a market bottom: efficient miners hold through downturns, while inefficient miners exit, tightening supply and supporting price recovery. The absence of large-scale miner capitulation suggests industry optimism and continued hashrate investment, reinforcing bullish price expectations.

2) Hashrate Growth Drivers

Hashrate’s entry into the ZH era is driven by:

- Large-scale expansions: Major mining firms are ramping up capacity.

- Riot: 31.4 EH/s avg hashrate in August, up 116% YoY, mining 477 BTC (+48% YoY).

- CleanSpark: 43.3 EH/s, up 103% YoY, mining 657 BTC (+37.5% YoY).

- Efficiency gains: Cheaper energy, better rigs, and higher efficiency are enabling sustained hashrate growth.

Result: record security levels (51% attack cost higher than ever) and strong miner confidence in BTC’s long-term value.

3) Cloud Mining Market

Cloud mining prices corrected slightly:

- Short-term (≤90d): ~-2% decline.

- 180d: stable.

- 360d: fell by >2%.

Cloud contracts remain competitive, especially in short-term offerings.

Average Cloud Mining Prices ($/T/day):

| Cloud Mining Product Term | Avg. Price ($/T/day) |

|---|---|

| 30 days | 0.055 |

| 60 days | 0.057 |

| 90 days | 0.057 |

| 120 days | 0.060 |

| 180 days | 0.059 |

| 360 days | 0.061 |

III. News & Events

This week, the macro policy environment showed a clear shift, with weak U.S. economic data reinforcing market expectations for monetary easing. On September 9, the U.S. Department of Labor released its annual benchmark revision for nonfarm payrolls, showing that over the year ending March 2025, U.S. nonfarm employment was revised down by 911,000, with a monthly average increase of 76,000, far below the market expectation of roughly 700,000, indicating that the labor market was significantly weaker than previously estimated.

Coupled with the latest August employment report, the U.S. added an average of only ~20,000 nonfarm jobs per month over the past three months, signaling rapid cooling in the labor market and raising concerns about an economic slowdown. Inflation-wise, August CPI rose 2.9% YoY and core CPI rose 3.1% YoY, both in line with expectations; month-over-month CPI rose 0.4%, slightly above the 0.3% forecast, suggesting modest inflationary rebound. However, production-side pressures eased — August PPI fell 0.1% MoM, with YoY growth slowing to 2.6%. The combination of broadly in-line or lower-than-expected inflation and weakening employment has been interpreted by markets as justification for the Fed to pivot toward easing sooner.

After the CPI release, the U.S. 10-year Treasury yield briefly fell below 4%, and initial jobless claims surged to 263,000, above the expected 235,000. Interest rate futures show a >90% probability of a 25bps cut at the September 20 Fed meeting, with some traders even betting on a single 50bps cut. The market generally expects the Fed to begin a rate-cut cycle this month, with a total reduction of around 0.75% by year-end. Expectations of macro easing have boosted BTC and other risk assets, with spot BTC breaking previous resistance levels amid inflows.

In the crypto industry, significant milestones were reached in digital asset investment products. The first-ever Dogecoin ETF (ticker: DOJE) was approved in the U.S. and will be listed, becoming the first U.S. exchange-traded fund targeting a single "meme" cryptocurrency. Analysts view this as largely symbolic, likely attracting retail investors with limited institutional participation. Meanwhile, the U.S. SEC continues to delay rulings on multiple crypto ETF applications, including ETH staking yield products and ETFs tracking Solana, XRP, and others, indicating that regulatory caution remains and approvals for spot ETFs on major coins continue to face repeated hurdles.

Regarding policy and regulation, legislative debates over crypto market oversight remain intense in the U.S., with some crypto-friendly bills stalled due to partisan disagreements. In Europe, MiCA regulations are entering implementation preparation, with mining energy consumption and sustainability issues under scrutiny. No major new policies directly affecting Bitcoin mining were introduced this week.

Overall, macro tailwinds have injected confidence into the crypto market, and mining fundamentals continue to strengthen; however, regulatory uncertainty remains a medium- to long-term factor that could shape the industry, requiring investors to closely monitor global regulatory developments and ETF approval progress for their potential impact on the Bitcoin market and mining landscape.

{kind=link}